All this because Delong admitted mistakes he's made in the past. Murphy insists on seeing "irony" in Delong's admissions even though Delong does this every year. However, the best irony came at the end when it turns out that he was wrong on what Delong had admitted to:

"I don’t want to discourage DeLong (or any other Keynesians for that matter) from self-flagellation in the future, but am I wrong for finding this latest post somewhat ironic?"

UPDATE: Daniel Kuehn reports in the comments:

Nice going Bob. However, it got me into a little bit of the history to this whole "irony." What it comes down to is that Murphy recently lost a bet that we'd have galloping inflation by 2013. He argued that it should change his ABCT theory about as much as picking the wrong team to win a football game would. He did also provide a longer piece of analysis.This just in to me from Brad:

The “I thought higher inflation would follow rather than precede recovery” is one of the 2 of 8 that I think I got right…

Yours,

Brad DeLong

He reasons that yes he lost the best but the bet was to David Henderson who's also a major Austerian so if one Austerian loses a bet to another it's no feather in Krugman's cap.

"Here’s the bigger context: Back in late 2008 and early 2009, many analysts–including me–were freaking out about the unprecedented actions that the Fed and other major central banks were taking. (For example, in June 2009 I explained why I thought the real economy would be “in the toilet for a decade” and that I expected “20+ percent price inflation.”) Bryan Caplan thought we were overreacting, and wanted to bet on something specific, so that the inflation-mongers couldn’t just issue vague warnings that might someday come true. Understanding that he had a point about non-falsifiable hysterics, I bet Bryan $100 in 2009 that by January 2016, official CPI would rise 10% year/year."

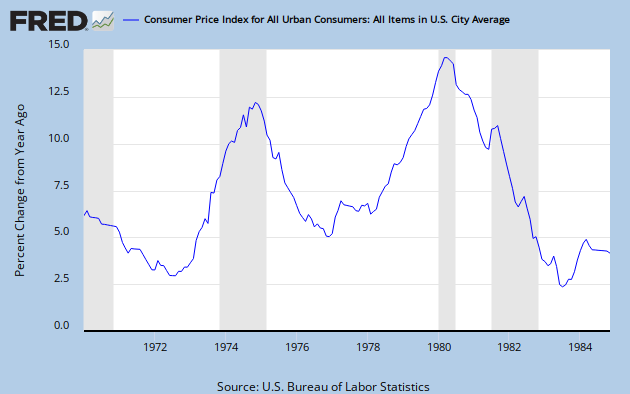

"Just to be clear–since these two points come up in every comment section on the issue–I was aware at the time that there are serious problems with the way the government calculates CPI, and I knew that if I won the bet, I would be getting paid in weaker dollars than if Bryan won. (I understand that rising prices means a weaker dollar, yes, I do understand that.) Official CPI inflation rose at almost 15% yr/yr at one point in the early 1980s, and since I think what Bernanke has done will ultimately be worse, I am thinking the government won’t be able to get away with reporting less than a double-digit rise."

{kind=link}

"Seeing my bet with Bryan, David wanted a piece of the action, but he wasn’t comfortable giving such a big window. So he wanted to shorten the horizon from January 2016 down to January 2013, and bump up the amount from $100 to $500. Obviously I was less confident about this bet than the one with Bryan, but I still thought I would win it so I said sure."

Murphy argues that ultimately this no more falsified ABCT than Krugman concedes that Keynesianism was falsified by Christina Romer and Jared Bernstein's erroneously optimistic predictions prior to the stimulus. Parenthetically,he also suggests that the stimulus might have had something to do with the failed predictions which makes no sense to me. Essentially no mainstream economists at the time were aware that the economy was already losing 750,000 jobs per month. The effects of the stimulus logically didn't start being felt until around February 2010.

So where does Bob think he went wrong in his 20% inflation prediction?

"I’m not sure yet, which is why I haven’t performed seppuku as DeLong insists. I realized that there were a lot of excess reserves when I made the bet with David, but it was also true that M1 had risen strongly since the onset of the crisis (presumably as people fled to very liquid assets). The big thing is that I did not, and do not, trust Bernanke when he tells us there will be a gentle unwinding of the Fed’s balance sheet, and that if things ever started getting out of hand he has all sorts of “exit strategies.” I thought other investors would eventually agree with me that the Fed was simply printing money to buy time and temporarily stave off disaster, and they’d head for the exits. Back in late 2009, I was sure enough that this would happen within two years that I bet $500 on it."

"Well, it hasn’t happened yet, so what does that mean? Are we stuck in a dollar and Treasury bubble that is taking longer to pop than I thought? Or have I been “completely, comprehensively, unmistakably, fundamentally, fatally, totally wrong,” as Gentle Brad puts it?

"I don’t know, of course, and none of us can, until the bubble bursts or the Fed unwinds its balance sheet with no major hiccups. So I haven’t been writing much on price inflation in a while, and when people ask me in radio interviews etc., I have been prefacing my remarks with, “Let me just admit, I thought this was going to happen already and it hasn’t, so take my analysis with that caveat…”

The main thing is that ABCT is unscathed according to him. He argues that Krugman-and by implication other mainstream econoimsts-don't get ABCT:

"I n any event, Krugman is hardly qualified to be telling us the empirical implications of Austrian theory. In his last written response to me, Krugman asked, “Why is there overwhelming evidence that when central banks decide to slow the economy, the economy does indeed slow?” To be clear, Krugman thought this would embarrass the Austrians, who must not have been aware of the peer-reviewed, cutting edge research showing that when central banks raise interest rates, the boom turns into a bust. This would be like asking a Christian, “Well if God loves us so much, why did He send His son?”

"The problem here is that Krugman actually hasn’t read much of Austrian business cycle theory. I’m guessing–can’t prove it–that he read somebody else summarizing it. This is why Krugman apparently classified it as a “real” theory, relying on underlying technological considerations, as opposed to Krugman’s demand-based theory. Since the central bank raising interest rates doesn’t burn crops or kill workers, Krugman thinks the Austrians must not be able to explain how changes in money can affect the business cycle."

"Anyway, if you want to see me give a point-by-point response to Krugman’s erroneous understanding of Austrian business cycle theory, read this essay."

I should say that I myself did read this essay and it is very interesting. That doesn't mean it's right. However, Murphy argues that Krugman doesn't know much firsthand about ABCT, that he essentially doesn't understand it's capital theory, simply presuming it's purely supply side; according to Bob ABCT should not be misconstrued with RBCT.

He then goes on to point out Krugman's misses through the years. There's really nothing shocking about this-what makes a good economist is surely not merely being a flawless prediciton machine as Bob himself understands. Still, admittedly Krugman does have some interesting predictions form the past where he urged to inflate the housing bubble.

Krugman’s notorious 2002 call for Greenspan to replace the bursting tech bubble with a housing bubble. Then, just to be sure there was no misunderstanding, read the 2006 exchange with a reader to see Krugman’s nuanced view of the matter. Having had to explain this extremely unfortunate statement many many times, Krugman has learned to no longer make flippant remarks about the Fed creating an asset bubble to prop up aggregate demand.

He also caught Krugman in 2008 aruging that the housing bubble had nothing to do with the recession. In this, Krugman and Sumner actually see eye to eye.

"In late 2008 Krugman argued that the housing bust had little to do with the recession, because the latest BLS figures showed that unemployment at the state level bore little relationship to the declines in home prices across the states."

I've now gotten into this collection of essays over at the Mises website. I'll be going back there again so I probably won't blog again this afternoon. Sometimes you got to do research. In explaining the waning of Austrianism in the 30s, I think they put well the choice between Keynes and Austrianism:

" Haberler concludes his essay with an expression of concern about the complexity of the Austrian theory, which he saw as a "serious disadvantage" (p. 64). But the complexity, in his judgment, is inherent in the subject matter and hence is not a fault of the theory. Complexity is evident in the two early essays (1936 and 1932) in their organization and style of argument. Both Mises and Haberler defend the theory against its critics and deal with various misunderstandings. Mises, for instance, identifies Irving Fisher's inflation premium, which attaches itself to the rate of interest as prices in general rise, only to say that this is not what he is talking about. He is discussing, instead, still another aspect of interest-rate dynamics. The real rate of interest rises at the end of the boom to reflect the increasing scarcity of circulating capital, after excessive amounts of capital have been committed to the early stages of production processes (p. 31). Haberler takes great pains to refocus the reader's attention away from the general price level and toward the relative prices that govern the "vertical structure of production" (p. 49). He distinguishes between "absolute deflation" and "relative deflation," and between "primary and fundamental" phenomena that characterize the downturn and "secondary and accidental" phenomena that may also be observed. All these complexities--plus still others involving such notions as the natural rate of interest and the corresponding degree of roundaboutness of the production process--are unavoidable in a theory that features an intertemporal capital structure. The theoretical richness that stems from the attention to capital has as its negative counterpart the expositional difficulties and scope for misunderstanding.

"Keynes offered the profession relief from all this by articulating--though cryptically--a capital-free macroeconomics. As Rothbard's discussion implies, all the thorny issues of capital theory were simply swept aside. An alternative theory that featured the playoff between incomes and expenditures left little or no room for a capital structure. Investment was given special treatment not because of its link to future consumption but because spending on investment goods is particularly unstable. Uncertainties, which are perceived to be a deep-seated feature of market economies, dominate decision making in the business community and give play to psychological explanations of prosperity and depression. And the notion that depression may be attributable to pessimism on the part of the business community suggests a need for central direction and policy activism. Prosperity seems to depend upon strong and optimistic leadership in the political arena. Relief from the complexities of capital theory together with policy implications that were exceedingly attractive to elected officials gave Keynesianism an advantage over Austrianism. An easy-to-follow recipe for managing the macroeconomy won out over a difficult-to-follow theory that explains why such management is counterproductive."

That says it all about the choice-no? Keynes gave them simple plan of how to manage the economy over a complex theory whose punchline is that the economy can't be managed.

That's it for now. Have a good Tuesday and let's hope the Yanks were just kidding yesterday. Some have pointed out that Sabbathia lost his first game in 2009 as well-and we know how that turned out: the Yankees won the world series. Of course, had he won yesterday we'd be worrying that his win is a bad omen for the season as when we won last time he lost his first start-right?

Of course not.

For the record, in 2009, I predicted low CPI inflation for many years because Fed policy would cause a long recession and the "inflation" would be channeled into artificially propping up the prices of assets that should have and would have naturally fallen. The concept of Cantillon Effects escapes you.

ReplyDeleteFurther, in 2002 Krugman said that,

"Alan Greenspan needs to create a housing bubble to replace the Nasdaq bubble."

http://www.nytimes.com/2002/08/02/opinion/dubya-s-double-dip.html

In 2005, Krugman admitted that the Fed had created a housing bubble and that it wasn't surprising because...

"After all, the Fed's ability to manage the economy mainly comes from its ability to create booms and busts in the housing market."

http://www.nytimes.com/2005/05/27/opinion/27krugman.html

But by 2010 Krugman completely changed his story and tried to absolve the Fed by saying...

"These considerations suggest that it would be wrong to attribute the real estate bubble wholly, or even in large part, to misguided monetary policy."

http://www.nybooks.com/articles/archives/2010/sep/30/slump-goes-why/?pagination=false

It is also clear that you do not understand basic Austrian concepts or analysis.

And then by 2012 Krugman started flat-out lying about what he said in the past by claiming he "never bought the story" that the Fed was the cause of the Housing Bubble. I guess it was the other Paul Krugman at the NYT who wrote that column in 2005.

ReplyDeletehttp://www.youtube.com/watch?v=KrfRS07CAHc ( video: 32:40 mark )

And most recently Krugman has said that the housing bubble was "just one of those things that happens" every once in a while.

http://www.youtube.com/watch?v=PD-EWxl_s4o&feature=plcp

Bob flattery will get you everywhere. I said that Austrianism is a complex theory of why government intervention doesn't work. Which part do you disagree with?

ReplyDeleteBy the way, after reading Krugman's piece it's not nearly as bad as you and Bob Murphy make it sound.

ReplyDeleteHe didn't call for a market bubble but he did clearly think more was needed.

Hey Mike

ReplyDeleteOff the topic of this post but I found something that might explain Mr Sumners crowing about success in Britain a few posts back.

http://www.telegraph.co.uk/finance/jobs/9968124/Number-of-Britons-on-zero-hours-contracts-hits-record-high.html

What an innovation!! A contract for a worker that guarantees nothing!....... except that they wont be officially counted as unemployed anymore so we can crow about out "employment growth numbers".

Man Im glad these business school types are putting their Masters and Phds to work so well. Who would have ever thought, prior to 2012, of using this type of scheme...... err.....

brilliant innovation to solve our employment problems!!

Great to see these great minds arent wasting their education and not just repackaging some worn out and discredited ideas from a few thousand years ago. I mean really...... can you even conceive of say...... an Egyptian Pharoah figuring a way to force someone to work for him...... whenever he wants and not promising anything in return.

Fascinating. Well zero hour contracts are an improvement over drafts (which also successfully eliminate unemployment). On a serious note, this is the issue with focusing on statistics that can be easily manipulated to show what is politically preferable. That's why employment-to-population figures are probably a better representation (though there are ways around this too).

DeleteNot sure how much I can add here. Murphy was clearly wrong, but one could point to countless non-Austrian mainstream economists who believe that the Fed's balance sheet expansion either would or still will create significant inflation (once banks release the reserves).

ReplyDeleteThere are clearly a number of things wrong with ABCT, but the same can be said of most (mainstream) theories. New Keynesians are getting better at understanding the bust but still have no consistent, coherent version of why the bubble happened (and maybe don't care).